clawock

Health Warn

- No license — Repository has no license file

- Description — Repository has a description

- Active repo — Last push 0 days ago

- Low visibility — Only 5 GitHub stars

Code Pass

- Code scan — Scanned 12 files during light audit, no dangerous patterns found

Permissions Pass

- Permissions — No dangerous permissions requested

No AI report is available for this listing yet.

Multi-agent LLM analysis on a real HK + US stock portfolio: a bull-vs-bear debate every morning, hard risk gates, and a daily scorecard that grades the AI's own calls — and admits it loses to buy-and-hold. Live dashboard, fully autonomous.

📈 clawock

An LLM swarm that watches my real HK + US money every trading day — and grades itself the next morning.

🎯 Live Dashboard · 📅 Daily Briefs · How it works ↓

English · 简体中文

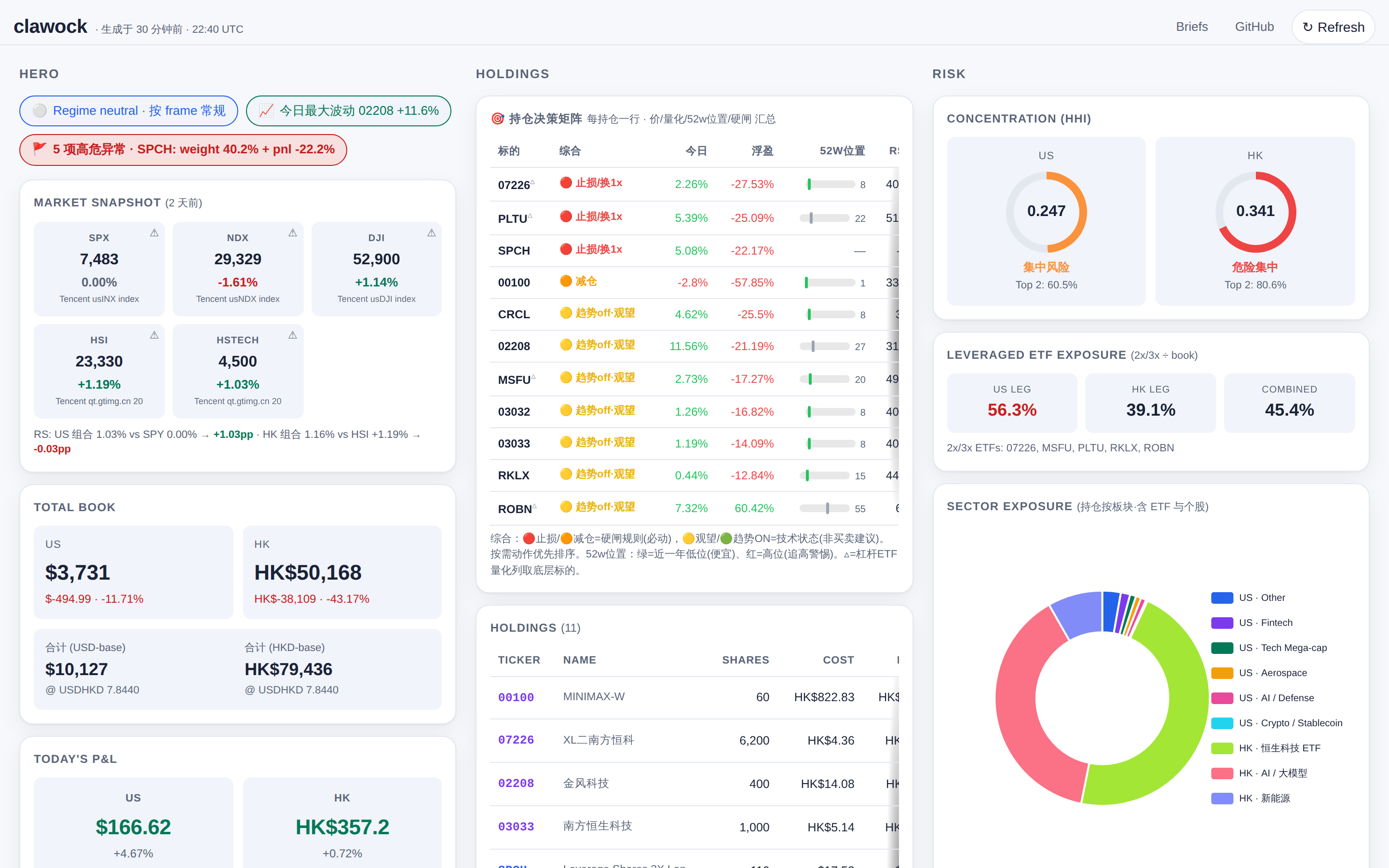

Real positions. Real P&L. The page updates after every cron run; this screenshot refreshes weekly via a GitHub Action so it never drifts.

🪞 Grades its own trades — and admits they lose to buy-and-hold · 💸 Real money, not a paper sim · 🗣️ Bull-vs-bear AI debate every morning · 🛡️ Python does the math — unit-tested, so the LLM can't fudge the score · 🌏 Bilingual HK + US · 🌐 Live public dashboard

If "an AI that's honest about being wrong" is your kind of thing — ⭐ it.

TL;DR — A multi-agent LLM runs a real Hong-Kong + US stock portfolio, debates bull-vs-bear each morning, and back-tests its own calls every night. Its verdict on itself, in public: the active calls lose to simply holding. The honesty is the point.

🎰 The 60-second version

I gave an LLM a real brokerage portfolio — a Hong Kong leg and a US leg, actual money — and wired up a small machine around it.

Every trading day, on its own, the system:

- 🌅 wakes up ~10 times (HK open, mid, close → US open, intraday, overnight, close),

- 📥 pulls fresh prices, FX, volatility, earnings calendars, macro (VIX/DXY/10Y), Reddit + news sentiment, even Trump/Musk market-movers,

- 🧠 hands the clean data to the best-available LLM — playing a blunt persona named Rick — to write the take,

- 📲 pushes a briefing to my WeChat, and

- 🌐 refreshes a public dashboard you can open right now.

That's the gimmick: a whole AI desk that trades alongside me and never sleeps.

But here's the part most "AI trader" demos skip 👇

🪞 It grades its own homework — and admits it's losing

Every brief doesn't just talk. It commits a structured plan.json: each call gets a trigger, a confidence number, and a simulated entry price. The next morning the system reads it back, checks which triggers actually fired, simulates the P&L, and logs the result to a rolling scorecard.

So I can tell you, with receipts, how the AI is actually doing:

| What the AI did | Sample | Hit rate | Honest verdict |

|---|---|---|---|

| cut / trim / add (active calls) | — | < 45% | worse than a coin flip |

| high-conviction calls (confidence ≥ 0.75) | — | 42% | overconfident |

just hold |

— | 76% | this is β, not α |

| 🔴 "chasing a high" warning | n=22 | 50% | flags the move, can't time it |

| 🟡 "oversold, might bounce" | n=77 | 36% | catching knives |

Read that again: on this sample, the model's active signals underperform simply holding. The system says so itself, in public, because the scorecard is computed in Python and the LLM isn't allowed to fudge it. The honesty is the feature — most of the value of an "AI analyst" is knowing when to ignore it.

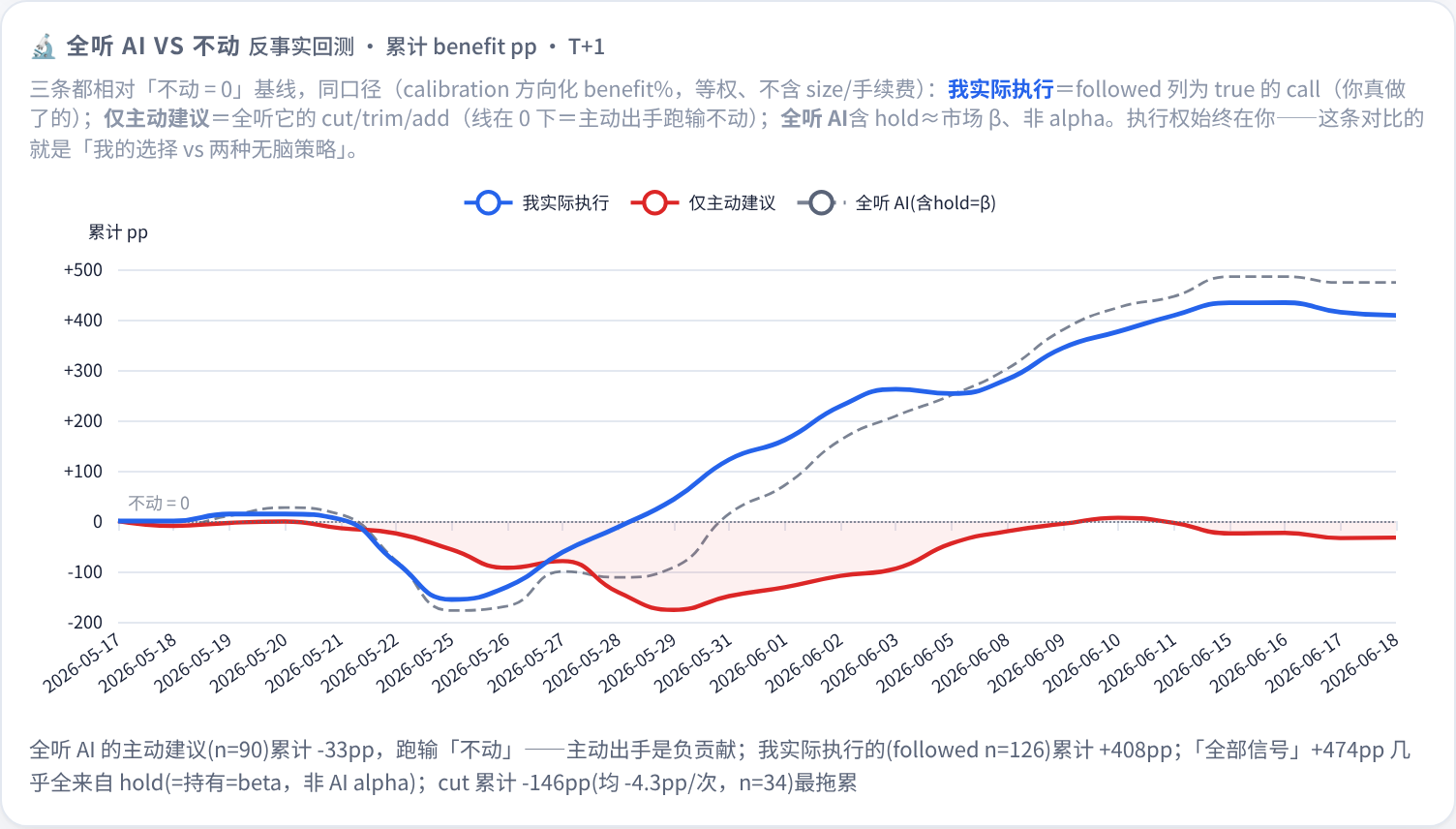

There's now a curve for it. A counterfactual "if you'd followed every call" backtest (the LLM only advises — execution is always mine) reuses the same direction-signed benefit% the scorecard already logs, and plots three lines against a do-nothing = 0 baseline on the Reflect tab: what I actually followed, follow-only-active, and follow-everything. The active-only line sits −33pp below doing nothing (T+1; −46pp at T+5); the "all signals" line's +474pp is almost entirely hold = market β; and what I actually did tracks that beta (I mostly held) — so you can see my real path against both naive policies, and watch the active calls bleed relative to a hold.

Numbers are point-in-time from memory/calibration.csv, quant_signal_review.json, t0_setup_review.json and move as samples grow. Factors with n < 20 are shown but barred from influencing decisions until they earn it.

The scorecard is built not to fool itself. Three guards stop a noisy number from masquerading as edge:

- 95% confidence intervals on every rate. "catalyst 72%" is really

[59–82]at n=54; a band that straddles 50% (macro, peer) is flaggededge_significant: false— statistically indistinguishable from a coin flip. - A risk-adjusted verdict, not just hit-rate. By frequency the active book looks +6pp ahead of holding. By return it's −0.57pp — and the gap isn't significant — against a portfolio β of 4.4. So a leveraged-beta "win" is never mistaken for skill.

- Catalyst-gate discipline. Only

catalysthas a CI-proven edge, so an active cut/trim/add must name the hard catalyst that justifies it (and the one that would invalidate its thesis). The dashboard tracks how many actually do — currently ~20%, i.e. most active calls are still filter-grade technicals.

🎯 How it actually decides

Behind the persona is a fixed decision framework — not freeform vibes. Every call is attributed, gated, and bucketed before it's allowed to count.

1. Attribution-first — and the edge is measured. Every call is tagged by what drove it, then scored over time. On the live record:

| Driver | Hit rate | How it's used |

|---|---|---|

| catalyst (earnings, FOMC, dated event) | 69% (n=61) | the only driver allowed to initiate an action |

| technical (trend / RSI / levels) | 59% (n=116) | a filter, never the thesis |

| macro | 50% (n=20) | context; a coin-flip on its own |

| peer / 抱团 read-across | 40% (n=10) | the worst — herd reasoning is actively distrusted |

2. Hard catalyst vs. soft sentiment. Soft sentiment (Reddit, mood, a single tweet) can only nudge a confidence number — it can never flip the action bucket. Only a hard, dated catalyst can.

3. Falsify, don't confirm. In a risk-on tape the default is HOLD. A confirming bullish story doesn't trigger a buy; the model first has to clear a disconfirming check and a "is this already priced in?" test (the last-5-day move).

4. Conviction is capped by hard risk gates. However sure it feels: single name ≤35%, Top-2 ≤70%, leverage-ETF sleeve ≤50%, portfolio β ≤3.0, stop at −18%. Position size is bounded by construction, not by mood.

5. Leverage is dialed by regime, not timed. A 200-day-trend × volatility dial sets a multiplier (×1 / ×0.5 / ×0) on the leverage-ETF cap. The backtest lesson behind it: the alpha was in de-leveraging in the wrong regime, not in calling tops.

6. Quant signals must earn the right to speak. A factor layer (MA cross, 12-1 momentum, RSI-14, z-score, ATR chandelier stop, vol-target sizing) runs in Python — but each factor is barred from influencing a decision until it clears n≥20 and proves a hit rate. Unproven factors are shown, never obeyed.

Everything resolves into an action bucket with an explicit trigger — cut / trim-on-rebound / hold / T-only / add-only-on-trigger. That bucket list is the plan.json graded the next morning: the strategy and the scorecard are the same object.

🗣️ Every morning, the desk argues with itself

The 08:00 deep brief isn't one model's monologue — it's a structured multi-agent debate, borrowed from TradingAgents and adapted for a dual-leg book:

- Tier 1 — four analyst lenses. Fundamental / technical / sentiment / sector-rotation each read the same

context.jsonand merge into one table. Numbers only, no vibes. - Tier 2 — Bull vs Bear. Two researchers build opposing cases (hold/add vs trim/cut), each citing ≥2 concrete Tier-1 data points. The hard rule: they must genuinely disagree on at least one position — unanimous agreement means the debate failed and is thrown out.

- Tier 3 — three risk voices + a Judge. Aggressive, Conservative and Neutral each argue their corner; a Judge weighs them, names which strategy frame is driving each decision, and resolves the argument into concrete bucketed actions with triggers.

The goal isn't consensus — it's forcing a real bear case to exist before anything is held, so the book never just talks itself into its own positions. The Judge's verdict is the plan.json that gets graded the next morning.

📅 What a day actually looks like

03:00 🌙 memory "dreaming" — promote yesterday's lessons into long-term notes

08:00 📊 daily deep brief — multi-tier analysis + a judge model, ships to WeChat

09:30 🇭🇰 HK open → 10:00–11:30 / 14:00–15:30 intraday → 12:00 mid → 16:00 close

21:30 🇺🇸 US open → 22:00–02:30 intraday (incl. overnight) → 04:00 close

↑ every run also refreshes the public dashboard

weekend 🛰️ macro / sentiment / influencer / news scans keep the page warm

All times HKT. Markets closed? A holiday + weekend gate skips the run instead of burning tokens and writing a stale price as if it were live.

🛡️ Why it doesn't quietly break

Running real automation for months taught me that the hard part isn't the prompt — it's everything that goes wrong around it. Three ideas carry the whole thing:

|

1. Harness pattern Every job is |

2. Self-learning loop

|

3. Defense in depth Four independent layers — cron → GitHub Action backstop → system-crontab watchdogs → health sentinels. A single LLM stall, a missed cron, or a flaky data source never silently drops a report. |

Models. Interactive chat runs on Claude (via the claude-cli runtime, reusing my Claude Code login — no key in the repo). The unattended briefs/reports run on a pinned MiniMax-M3 with a fallback chain behind it (GLM → DeepSeek → GPT → Claude → Haiku). Mixed protocols: Claude/MiniMax speak anthropic-messages (thinking is its own block); GLM/DeepSeek/OpenAI speak openai-completions. A third-party reasoning model must be registered with "reasoning": true or its thinking silently locks off — a trap I paid for once.

Write reconciliation (the one genuinely hard part). dashboard.json is 100% derived, yet many jobs touch master — the cron daemon, ~11 GitHub Actions, system-crontab backstops, ad-hoc sessions. Months of race-condition incidents converged on one rule: one writer per file.

- The frontend reads the scan sidecars directly.

macro / sentiment / influencer_feed / us_news_digest / em_newsare no longer embedded intodashboard.json;index.htmlfetches each file itself at load. So a GitHub Action only ever commits its own disjoint sidecar — those writers can't conflict, and a scan appears on the page the instant its commit lands, with no rebuild. (GH Actions still serialize among themselves viaconcurrency: group: data-write.) dashboard.jsonhas exactly one publisher path. Only the local harness postflights and a flock-guardedpublish_dashboard.shcrontab rebuild it; both hold the same/tmp/dashboard_publish.lock, so two rebuilds can never interleave. The publisher re-commits only on a semantic diff (wall-clock fields stripped), so a freshness tick alone never spams a no-op commit.- Everyone pushes through

safe_push.sh— rebase-retry, abort (don't loop) on a real conflict; a committed conflict marker is rejected at the push hook so a brokendashboard.jsoncan never reach Pages. - Portfolio numbers are gated at the door.

portfolio.json— the single source of truth — is written under an advisoryflock+ read-fresh-then-overlay (mutate_json, atomicos.replace), closing the load-modify-write race class. A pre-push hook blocks any push whose book fails a money-conservation identity (TCV = Σ value,cash = baseline + trades + adjustments,cost = moving-weighted), so an un-reconciled edit can't reach Pages — and those pure derivations are pinned by apytestsuite in CI.

📐 House rules the code enforces

The constraints postflight won't let the model violate. Quant readers will recognize why each exists:

- 🪙 FX — HKD and USD never sum directly. Totals are always shown in both views with the rate + timestamp stamped (

USDHKD = 7.83, source Frankfurter, <ts>). Adding two currencies naively is a meaningless number. - 🔢 Manual-entry guards. The few hand-typed values (cash balances, gold-fund reconciliation) get fat-finger checks: a cash number that jumps ≥5× vs the last snapshot, or a gold avg-cost that diverges from NAV, is flagged before it silently corrupts total assets.

- 📊 Concentration — HHI per leg.

HHI = Σ wᵢ², plus Top-2 weight. Buckets:<0.15✅ ·0.15–0.25🟡 ·0.25–0.40🟠 ·>0.40🔴. Computed per leg, never blended. - 🎲 Leverage ETFs — judge the underlying. Tickers whose name carries a leverage marker (

倍,Direxion,T-Rex,ProShares,2X/3X Long, …) skip fundamentals entirely — for a daily-reset 2×/3× product, fundamentals are noise; a regime dial (200-day trend × volatility) caps how much leverage is allowed instead. - 💵 Return basis — peak net principal. Return % uses

true_principal= peak net deposit from the cash-flow ledger, notcost − realized. A realized win shrinkscost − realizedand fakes a higher return; the ledger basis doesn't move.

🧬 Stack & sources

Claude Code · openclaw (cron daemon) · ECharts 5.5 · Jekyll + GitHub Pages · Python 3.11 · pure-static frontend

Public data Tencent · stooq · yfinance · Frankfurter · SEC EDGAR · Finnhub · Nasdaq · Eastmoney · Polygon · Alpha Vantage · Reddit JSON · Google News RSS · Trump Truth Social feed

The news layer is deliberately bilingual: Finnhub + Google News (English/US) and Eastmoney company news + 7×24 快讯 (Chinese/HK), since half the book is Hong Kong and HK catalysts surface in Chinese sources first. Information breadth is the one axis kept wide on purpose — it's what an LLM is best at — separate from the deliberately-narrow decision layer.

📂 Repository layoutclawock/

├─ index.html briefs.md ← Pages landing

├─ assets/data/ built by harness + GH Actions, never hand-edited

│ ├─ dashboard.json risk.json catalysts.json fx.json

│ ├─ macro.json sentiment.json influencer_feed.json us_news_digest.json ← scan sidecars, fetched straight by the frontend

│ ├─ quant_signals.json quant_signal_review.json ← factor scorecard

│ └─ t0_setups.json t0_setup_review.json ← intraday setup scorecard

├─ portfolio.json ← single source of truth (atomic writes)

├─ tests/ ← pytest: money-conservation derivations (CI-gated)

├─ MEMORY.md DREAMS.md ← iron rules + nightly "dreaming" promotion

├─ memory/

│ ├─ {date}-pre-open.md {date}-plan.json ← brief output + structured plan

│ ├─ calibration.csv ← the self-grading scorecard

│ └─ snapshots/{date}.json

├─ scripts/

│ ├─ data/ fetchers · build_dashboard.py · risk/quant/regime/t0 compute · safe_push.sh

│ └─ harness/ {brief,report,intraday}_{pre,post}flight.py · watchdogs

└─ skills/{name}/SKILL.md

⚠️ Disclaimer

This repo contains real, live trading positions — that's the whole point of sharing it, and also the reason to take everything in it with a fistful of salt. It is a personal record and a portable workspace. It is not investment advice, not a recommendation, and not something you should copy — the scorecard above literally shows the active calls underperforming a hold. Every number is point-in-time and may be stale by the time you read it. Rick is opinionated by design; that doesn't make him right.

📄 License

Personal-use repository. No license granted for derivative trading systems, automated copy-trading, or commercial use. The patterns (harness layout, fallback-chain design, HHI formulation, atomic IO, the self-grading loop) may be adapted under any compatible open-source license if reused independently.

⭐ Star it if "an AI that's honest about being wrong" is your kind of thing.

🎯 Live Dashboard · 📅 Daily Briefs · 简体中文

Built and maintained by Shengyu Li (kcn) and Rick · 2026

Reviews (0)

Sign in to leave a review.

Leave a reviewNo results found