awesome-quant-ai

Health Gecti

- License — License: Apache-2.0

- Description — Repository has a description

- Active repo — Last push 3 days ago

- Community trust — 191 GitHub stars

Code Uyari

- Code scan incomplete — No supported source files were scanned during light audit

Permissions Gecti

- Permissions — No dangerous permissions requested

Bu listing icin henuz AI raporu yok.

A curated list of awesome resources for quantitative investment and trading strategies focusing on artificial intelligence and machine learning applications in finance.

Awesome Quant AI

![]()

A curated list of awesome resources for quantitative investment and trading strategies focusing on artificial intelligence and machine learning applications in finance.

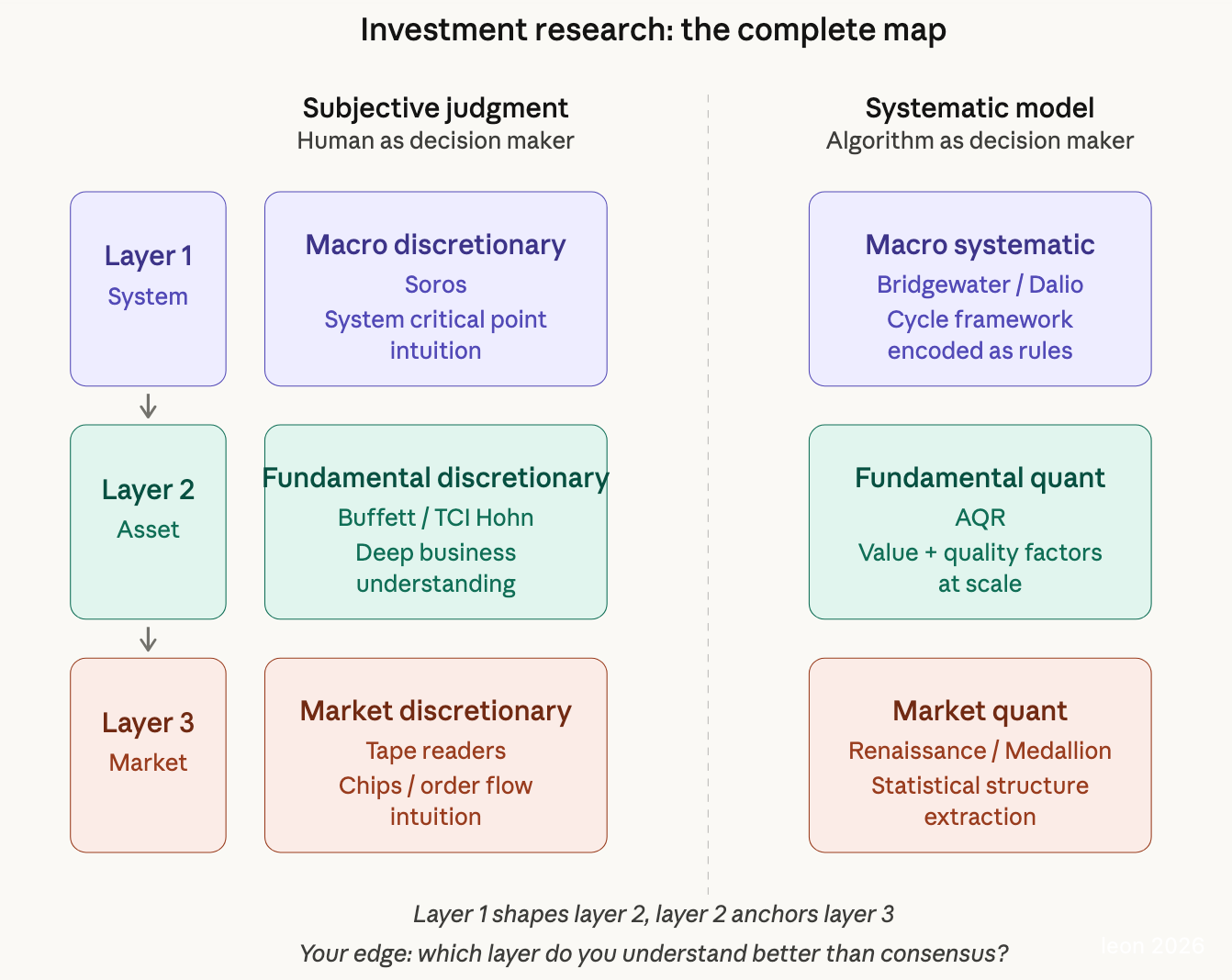

Your edge: which layer do you understand better than consensus?

Contents

- Introduction

- Design Approach

- Quantitative Trading Strategies

- Trading Paradigms Comparison

- Frontier: Emerging Topics (2025/2026)

- Tools and Platforms

- Learning Resources

- Books

- Research Papers

- Original Research and Notes

- Community and Conferences

- Related Lists

- Reference

- Contributing

Introduction

Quantitative investing uses mathematical models and algorithms to determine investment opportunities. This repository aims to provide a comprehensive resource for those interested in the intersection of AI, machine learning, and quantitative finance. At its core, this field addresses three pillars:

Key Challenges in Quantitative Finance:

- Efficient Market Hypothesis (EMH): Balancing the tension between market efficiency and exploitable inefficiencies through rigorous statistical testing.

- Factor Validity: Identifying persistent drivers of returns (e.g., value, momentum, quality) and assessing their decay over time due to overcrowding or regime shifts.

- Statistical Arbitrage Limits: Quantifying theoretical profit bounds under constraints like transaction costs, liquidity gaps, and execution latency.

- Cost Modeling: Integrating bid-ask spreads, slippage, taxes, and market impact into strategy design.

AI/ML Technical Fit:

- Predictive Modeling (Supervised Learning): Forecasting asset returns, volatility, and risk metrics using labeled data with techniques ranging from linear regression to advanced gradient-boosted trees (XGBoost, LightGBM).

- Pattern Discovery (Unsupervised Learning): Identifying latent structures in data through asset clustering, dimensionality reduction, and anomaly detection to uncover novel factors or market regimes.

- Sequential Decision-Making (Reinforcement Learning): Optimizing trading and execution policies through continuous environment interaction, using algorithms like PPO or DDPG to maximize risk-adjusted returns.

- Synthetic Data Generation (Generative Models): Utilizing GANs, Diffusion Models, and other generative techniques to create realistic market scenarios for robust strategy stress-testing and data augmentation.

- Contextual Reasoning (Large Language & Multimodal Models): Achieving a deep, semantic understanding of unstructured financial text, audio, and image data to decode complex informational alpha from filings, news, and earnings calls, far surpassing traditional sentiment analysis.

Mathematical Foundations:

- Stochastic Processes: Modeling price dynamics with Brownian motion, jump-diffusion, or fractional processes.

- Optimization Theory: Mean-CVaR frameworks for balancing returns against tail risks.

- Game Theory: Simulating strategic interactions among market participants (e.g., order-book competition).

Quant AI is the application of advanced computational methods to systematically extract alpha while rigorously managing risk in complex, adaptive financial systems.

Design Approach

A scientifically rational design for a quantitative trading system or strategy should adhere to the following process:

Define Objectives and Constraints:

- Specify investment goals (e.g., absolute return, relative return benchmarks, target risk levels).

- Clearly outline risk tolerance, available capital, constraints on trading frequency, and permissible markets and financial instruments.

Strategy Identification and Research (Alpha Research):

- Theory-Driven/Literature-Based: Draw inspiration from established strategy types (e.g., statistical arbitrage, factor investing, trend following) detailed in the source material or academic/practitioner literature.

- Data-Driven Discovery: Utilize statistical analysis, econometrics, or machine learning techniques (e.g., supervised learning for price prediction, unsupervised learning for factor discovery or regime identification, NLP for sentiment analysis) to explore data and uncover potential trading signals (Alpha).

- Signal/Strategy Combination: Consider combining multiple, ideally weakly correlated, alpha signals or distinct strategies (e.g., within multi-factor models or multi-strategy frameworks) to enhance portfolio stability and risk-adjusted returns (e.g., Sharpe Ratio).

Model Development and Calibration:

- Formalize the core strategy logic into specific mathematical models or algorithmic rules.

- If employing machine learning, select appropriate models (e.g., linear models, tree-based ensembles, neural networks, reinforcement learning agents) and conduct relevant feature engineering.

- Calibrate model parameters judiciously, employing techniques (e.g., regularization, cross-validation) to mitigate the risk of overfitting the training data.

Rigorous Backtesting and Validation:

- Conduct thorough backtests using high-quality historical data that accurately reflects market conditions.

- Realistically account for transaction costs (commissions, slippage) and potential market impact/liquidity constraints.

- Perform out-of-sample (OOS) testing and sensitivity analyses to assess robustness. Use cross-validation where appropriate.

- Evaluate performance using robust statistical metrics (e.g., Sharpe ratio, Sortino ratio, maximum drawdown, win rate, profit factor) and assess the statistical significance of the results. Consider methodologies like those proposed by Marcos Lopez de Prado to prevent backtest overfitting.

Integrate Robust Risk Management:

- Embed strategy-level risk controls (e.g., stop-losses, position sizing rules based on volatility or risk contribution).

- Apply portfolio-level risk management techniques (e.g., diversification, risk parity principles, asset allocation overlays, correlation monitoring).

- Develop contingency plans for managing exposure during extreme market events (tail risk / black swans).

System Implementation and Deployment:

- Select or develop the appropriate technological infrastructure (trading platforms, data feeds, execution systems).

- Ensure data integrity and low-latency, reliable execution capabilities (especially critical for higher-frequency strategies).

- Consider leveraging cloud computing resources for computationally intensive tasks (backtesting, model training) and deployment scalability.

Continuous Monitoring and Iteration:

- Post-deployment, continuously monitor live trading performance against expectations and track evolving market conditions.

- Periodically evaluate the strategy's efficacy and diagnose potential performance degradation or alpha decay.

- Based on monitoring feedback and ongoing research, systematically adjust, optimize, refine, or potentially retire the strategy. (Note: For AI-Agent trading paradigms, aspects of this monitoring and adaptation loop may be automated).

Quantitative Trading Strategies

1. Statistical Arbitrage

- Exploiting pricing inefficiencies among related financial instruments using advanced statistical models.

- Sub-strategies:

- Mean Reversion: Assuming asset prices will revert to their historical average.

- Pairs Trading: Taking long and short positions in correlated securities.

- Cointegration Analysis: Exploiting long-term price relationships.

2. Factor Investing

- Investing in securities that exhibit characteristics associated with higher returns, such as value, momentum, or size.

- Factors:

- Value: Selecting undervalued stocks.

- Momentum: Buying recent winners and selling losers.

- Size: Investing in small-cap stocks.

- Quality: Selecting stocks based on financial health indicators.

- Low Volatility: Investing in stocks with lower price fluctuations.

3. High-Frequency Trading (HFT)

- Rapid trading using powerful computers and algorithms.

- Approaches:

- Market Making: Providing liquidity by simultaneously placing buy and sell orders.

- Latency Arbitrage: Exploiting tiny price discrepancies.

- Order Flow Prediction: Anticipating and acting on order flow patterns.

4. Trend Following

- Trading based on the continuation of price trends.

- Methods:

- Moving Averages: Using price averages to identify trends.

- Breakout Trading: Entering positions when prices move beyond support/resistance levels.

- Momentum Indicators: Using technical indicators to measure price velocity.

5. Volatility Trading

- Strategies focused on market volatility rather than directional moves.

- Methods:

- Options Pricing: Using volatility models for options valuation.

- Volatility Arbitrage: Exploiting differences between implied and realized volatility.

6. Risk Parity

- Allocating capital based on risk, balancing the contributions of different assets to overall portfolio volatility.

- Implementation:

- Balancing Risk Contributions: Across different asset classes.

- Leveraging Lower-Risk Assets: To achieve the desired risk/return profile.

7. Quantitative Macro Strategies

- Trading based on macroeconomic factors and global market trends.

- Approaches:

- Global Macro: Trading based on broad economic trends.

- Asset Allocation: Dynamically adjusting portfolio composition based on market conditions.

8. Event-Driven Strategies

- Trading based on specific events or news.

- Examples:

- Merger Arbitrage: Trading around M&A activities.

- Earnings Announcements: Trading based on financial report releases.

- Economic Data Releases: Trading on macroeconomic news.

9. Machine Learning and AI Strategies

- Utilizing AI to improve human decision-making processes and improve investment strategies. Deploying algorithms to analyze vast datasets and enhance the accuracy and efficiency of financial models.

- Techniques:

- Supervised Learning: Predicting outcomes using labeled data.

- Unsupervised Learning: Discovering hidden patterns in data.

- Reinforcement Learning: Learning optimal strategies through environment interaction.

- Natural Language Processing (NLP): Analyzing text data for trading signals.

10. Multi-Strategy Approach

- Combining multiple strategies to diversify and enhance performance.

- Examples:

- Multi-Factor Models: Integrating multiple factors in a single strategy.

- Strategy Allocation: Dynamically allocating capital across various quantitative strategies.

| Category | Sub-directions | Technical Stack & Tools | Real-World Applications |

|---|---|---|---|

| AI-Enhanced Traditional Strategies | 1. Factor Investing: - SHAP feature selection for factor validity - Dynamic factor weighting calibration - Nonlinear factor fusion (XGBoost/GNN) 2. Statistical Arbitrage: - Cointegration + Graph Neural Networks - Kalman Filter for pairs trading 3. Trend Following: - CNN for candlestick pattern recognition (e.g., head-and-shoulders) - LSTM anomaly detection for trend reversal signals |

- Pyfolio (performance attribution) - Alphalens (factor testing) - Featuretools (automated feature engineering) - DGL (Graph Neural Network library) |

- Multi-factor equity selection systems (A-shares/US stocks) - Crypto cross-exchange arbitrage - Commodity futures trend tracking strategies |

| End-to-End AI Strategies | 1. Reinforcement Learning (RL): - DDPG/PPO for asset allocation - Deep Q-learning for order execution optimization 2. Transformer-Based Forecasting: - TimesNet for multi-scale volatility prediction - Informer for long-horizon price modeling 3. Multi-Agent Market Simulation: - DeFi liquidity - Adversary behavior inference |

- Stable Baselines3 (RL framework) - Hugging Finance (Transformers for Time Series) - PettingZoo (multi-agent training environment) |

- Adaptive options hedging (Black-Scholes) - Crypto market-making - Stress-testing under extreme market scenarios |

| Cross-Domain Emerging Fields | 1. Crypto Market Making: - Order-book state prediction (LSTM+attention) - MEV arbitrage path optimization 2. ESG Factor Quantification: - BERT for ESG report parsing - ESG-financial metric nonlinear modeling 3. Climate Risk Pricing: - Physical risks: Natural disaster data mapping to asset exposure - Transition risks: Carbon price sensitivity analysis + policy text mining |

- CoinMetrics (crypto data) - SASB standards (ESG metrics) - Bloomberg NEF (climate finance) - TensorFlow Probability (uncertainty quantification) |

- Carbon-neutral ETF dynamic rebalancing - Extreme weather-driven commodity strategies - Blockchain MEV extraction bots |

Trading Paradigms Comparison

Comparing three major approaches to quantitative trading: Quantitative Trading, Algorithmic Trading, and AI-Agent Trading.

| Feature | Quantitative Trading | Algorithmic Trading | AI-Agent Trading |

|---|---|---|---|

| Decision Process | Static rules based on mathematical models and historical data | Predefined algorithmic logic with optimization mechanisms | Autonomous learning and decision-making agents adapting to environment changes |

| Adaptability | Low, requires manual parameter and rule adjustments | Medium, self-adapts through parameter optimization | High, real-time learning and adaptation to market conditions |

| Market Understanding | Limited to pre-programmed rule scopes | Medium, can capture some complex patterns | Comprehensive, can understand and adapt to complex market structures |

| Learning Capability | None or limited | Based on supervised learning or parameter optimization | Autonomous learning and exploration abilities, can improve strategies through reinforcement learning |

| Flexibility | Low, fixed rules | Medium, adjustable algorithms but fixed frameworks | High, autonomous adjustment of strategies and objectives |

| Transparency | High, clear and explainable rules | Medium, higher algorithm complexity but traceable | Lower, decision processes may be "black box" |

| Risk Management | Fixed rule-based risk control | Built-in algorithmic risk control mechanisms | Dynamic risk assessment and adaptive risk management |

| Complexity | Low to medium | Medium to high | High, involving complex AI/ML models and architectures |

| Computational Requirements | Lower | Medium | High, especially during training phases |

| Data Dependency | Relies on specific types of historical data | Strong dependency on multiple data sources | Can process multi-dimensional, unstructured data including real-time feedback |

| Maintenance Cost | Lower, simple and stable rules | Medium, requires periodic adjustments and optimization | High, requires continuous monitoring and possible retraining |

| Innovation Potential | Limited by preset rules | Medium, achievable through algorithm optimization | High, can discover new trading strategies and opportunities |

| Typical Applications | Trend following, mean reversion, fundamental quantitative analysis | Statistical arbitrage, high-frequency trading, factor models | Adaptive trading systems, hybrid strategy optimization, multi-objective decision making |

| Recent Developments | Integration of more data sources | Introduction of machine learning to optimize algorithm parameters | Multi-agent collaboration, meta-learning, transfer learning applications |

Frontier: Emerging Topics (2025/2026)

LLM-Based Trading Agents

Multi-agent systems using large language models in specialized roles (analyst, trader, risk manager) to collaboratively process unstructured data and make trading decisions — representing a shift from fixed-rule systems toward autonomous, adaptive trading.

- TradingAgents - Multi-agent LLM trading framework simulating trading firm dynamics with specialized analyst and trader roles; built with LangGraph, supports GPT, Gemini, Claude, and Grok.

- FinRobot - Open-source AI agent platform for financial analysis using LLMs with Financial Chain-of-Thought reasoning and smart scheduler for multi-source LLM integration.

- FinGPT - Open-source financial LLM framework with data-centric design and LoRA fine-tuning; supports sentiment analysis, robo-advising, and algorithmic trading.

- FinRL - Financial reinforcement learning framework supporting A2C, DDPG, PPO, TD3, SAC agents; FinRL-X adds modular infrastructure for the LLM/agentic AI era.

Transformer Time-Series Foundation Models

Pre-trained transformer models for temporal data that can forecast time series zero-shot or few-shot — offering out-of-the-box price/volatility forecasting and regime identification without task-specific training.

- Chronos - Amazon's pretrained time series models; Chronos-2 (120M params) handles univariate, multivariate, and covariate-informed zero-shot forecasting.

- TimesFM - Google Research's decoder-only foundation model (200M params) pre-trained on 100B real-world time points.

- Moirai - Salesforce's masked encoder-based universal forecasting transformer, pre-trained on LOTSA (27B observations, 9 domains); handles any frequency and any number of variates.

- Lag-Llama - First open-source decoder-only foundation model for probabilistic time series forecasting; developed by Morgan Stanley, ServiceNow, and Mila.

- PatchTST - Segments time series into subseries-level patches as transformer tokens, achieving quadratic reduction in attention cost while retaining local semantics.

- TimeGPT - Production-ready foundation model trained on 100B+ data points with open-source Python/R SDK; offers zero-shot forecasting and anomaly detection via API.

Diffusion Models for Synthetic Financial Data

Denoising diffusion models applied to generate realistic synthetic market data — price series, order flows, and limit order books — enabling robust stress-testing and data augmentation for data-starved financial ML.

- DeepMarket - Transformer-based diffusion engine for limit order book simulation; generates realistic order flows conditioned on market state.

- FinDiff - Diffusion model for generating mixed-type financial tabular data; demonstrated high fidelity for downstream tasks like fraud detection and stress testing.

- FTS-Diffusion - ICLR 2024 scale-invariant diffusion framework for financial time series; reduces stock prediction error by up to 17.9% when used for data augmentation.

On-Chain / DeFi Quantitative Strategies

Quantitative approaches to decentralized finance: MEV extraction, AMM liquidity provision optimization, yield farming, and on-chain analytics across hundreds of chains.

- Flashbots mev-boost - Reference implementation of proposer-builder separation (PBS) for Ethereum; core infrastructure for the MEV supply chain.

- Flashbots rbuilder - Open-source, high-performance Ethereum MEV-Boost block builder written in Rust; supports multiple building algorithms and backtesting.

- DefiLlama - Open-source DeFi analytics dashboard tracking TVL, yields, fees, and volumes across thousands of protocols; provides free API via defillama-sdk.

- ultimate-defi-research-base - Curated collection of DeFi and blockchain research covering MEV, AMM design, yield optimization, and on-chain analytics.

Tools and Platforms

List of software tools and platforms used in quantitative finance.

- pytrade - Python packages and resources for algo-trading.

- pybroker - Algorithmic trading framework focused on strategies backtesting that use machine learning.

- KeepRule - AI-powered investment discipline platform with principles from 26 legendary investors including Buffett, Munger, and Dalio.

1. Strategy Development Frameworks

| Tool | Strength | Community Activity | Academic Adoption | Enterprise Use |

|---|---|---|---|---|

| Backtrader | Multi-factor strategy backtesting | High | Medium | Medium |

| Zipline | End-to-end trading pipelines | Medium | High | High (Quantopian) |

| QuantConnect | Cross-market support (stocks, crypto) | High | Medium | High |

| TensorTrade | Reinforcement learning prototyping | Medium | Medium | Medium |

| Ray/Rllib | Adaptive strategies in complex environments | High | High | High |

2. Data Providers

| Provider | Key Features | Use Cases |

|---|---|---|

| Alpha Vantage | Free APIs for stock/crypto data | Historical price/volume analysis |

| Quandl | Premium structured datasets | Macroeconomic/factor data integration |

| Yahoo Finance | Open-source financial data | Basic equity/ETF research |

| Bloomberg Terminal | Institutional-grade market data | High-frequency trading, ESG analytics |

| CoinMetrics | Crypto-specific metrics | On-chain transaction analysis, MEV tracking |

| FinancialData.Net | Stock market and financial data | Financial analysis, data integration |

| StockAInsights | Institutional-grade AI-extracted SEC financial statements (not XBRL) | Fundamental analysis, backtesting, screening |

3. Execution & Deployment

- Interactive Brokers API - Low-latency order execution for algorithmic trading.

- Alpaca - Commission-free algorithmic trading API with paper trading support.

- AWS SageMaker - Cloud-based ML training and deployment for quantitative models.

- Docker / Kubernetes - Containerization and orchestration for scalable trading systems.

4. Research Environments

- Jupyter Notebook - Interactive strategy prototyping and data exploration.

- Databricks - Big-data processing for alternative data streams and large-scale backtesting.

Learning Resources

Online courses, tutorials, and workshops focused on quantitative investing and machine learning in finance.

- Algorithmic Trading & Quantitative Analysis Using Python - Hands-on course covering Python-based algorithmic trading and quantitative analysis.

- Quantitative Trading Strategies (UChicago FINM 33150) - Graduate-level course on quantitative trading strategy design and implementation.

- Oxford Algorithmic Trading Programme - Executive education programme covering algorithmic trading fundamentals and practice.

- Princeton ORFE Financial Mathematics - Research and curriculum in financial mathematics from Princeton's ORFE department.

Books

Significant books in quantitative finance, algorithmic trading, and market data analysis. Each has proven invaluable for learning and applying quantitative techniques in the financial markets.

Trading Systems and Quantitative Methods

- Quantitative Trading: How to Build Your Own Algorithmic Trading Business by Ernest Chan - A great introduction to quantitative trading for retail traders.

- Algorithmic Trading: Winning Strategies and Their Rationale by Ernest Chan - Advanced strategies for developing and testing algorithmic trading systems.

- Machine Trading: Deploying Computer Algorithms to Conquer the Markets by Ernest Chan - Introduction to strategies in factor models, AI, options, time series analysis, and intraday trading.

- Mechanical Trading Systems by Richard Weissman - Discusses momentum and mean reversion strategies across different time frames.

- Following the Trend by Andreas Clenow - Insightful read on trend following, a popular quantitative trading strategy.

- Trade Your Way to Financial Freedom by Van Tharp - Structured approaches to developing personal trading systems.

- The Mathematics of Money Management by Ralph Vince - Techniques on risk management and optimal portfolio configuration.

- Intermarket Trading Strategies by Markos Katsanos - Explores global market relationships for strategy development.

- Applied Quantitative Methods for Trading and Investment by Christian Dunis et al. - Practical applications of quantitative techniques in trading.

- Algorithmic Trading and DMA by Barry Johnson - An introduction to direct market access and trading strategies.

- Technical Analysis from A to Z by Steven Achelis - A comprehensive guide to technical analysis indicators.

- Finding Alphas: A Quantitative Approach to Building Trading Strategies by Igor Tulchinsky - Discusses the process of finding trading strategies (alphas).

- Algorithmic and High-Frequency Trading by Alvaro Cartea, Sebastian Jaimungal, and Jose Penalva - Provides an in-depth understanding of high-frequency trading strategies.

- Building Reliable Trading Systems by Keith Fitschen - Focuses on developing trading systems that perform well in real-world conditions.

- Professional Automated Trading: Theory and Practice by Eugene A. Durenard - A practical guide to automated trading systems.

- Quantitative Investing: From Theory to Industry by Lingjie Ma - Bridges the gap between academic quantitative theory and industry practice.

- Trading Systems and Methods, 6th Edition by Perry J. Kaufman - The definitive reference on trading systems, covering technical analysis, arbitrage, and risk management.

Behavioral and Historical Perspectives

- Reminiscences of a Stock Operator by Edwin Lefèvre - Classic insights into the life and trading psychology of Jesse Livermore.

- When Genius Failed by Roger Lowenstein - The rise and fall of Long-Term Capital Management.

- Predictably Irrational by Dan Ariely - A look at the forces that affect our decision-making processes.

- Behavioral Investing by James Montier - Strategies to overcome psychological barriers to successful investing.

- The Laws of Trading by Agustin Lebron - Decision-making strategies from a professional trader's perspective.

- Thinking, Fast and Slow by Daniel Kahneman - A classic on human decision-making and cognitive biases, crucial for understanding market behavior.

- The Undoing Project by Michael Lewis - Chronicles the collaboration between Daniel Kahneman and Amos Tversky and their contributions to behavioral economics.

Statistical and Econometric Analysis

- Machine Learning for Algorithmic Trading by Stefan Jansen - Techniques for developing automated trading strategies using machine learning.

- Advances in Financial Machine Learning by Marcos Lopez de Prado - Discusses the challenges and opportunities of applying ML/AI in trading.

- Machine Learning for Asset Managers by Marcos Lopez de Prado - Focuses on portfolio construction, feature selection, and identifying overfit models.

- Time Series Analysis by James Hamilton - Statistical methods for analyzing time series data in economics and finance.

- Econometric Analysis by William Greene - A fundamental textbook on econometric methods.

- Wavelet Methods for Time Series Analysis by Donald Percival and Andrew Walden - Utilizes wavelet analysis for financial time series.

- The Elements of Statistical Learning by Hastie, Tibshirani, and Friedman - A comprehensive overview of statistical learning theory and its applications.

- Applied Econometric Time Series by Walter Enders - Demonstrates modern techniques for developing models capable of forecasting, interpreting, and testing hypotheses concerning economic data.

- Data-Driven Science and Engineering: Machine Learning, Dynamical Systems, and Control by Steven L. Brunton and J. Nathan Kutz - Focuses on the application of machine learning in scientific and engineering contexts.

- Big Data and Machine Learning in Quantitative Investment by Tony Guida - Explores the role of big data and machine learning in quantitative investment.

- Big Data Science in Finance by Irene Aldridge and Marco Avellaneda - Provides insights into the application of big data science in the financial industry.

- Machine Learning and Data Sciences for Financial Markets: A Guide to Contemporary Practices by Agostino Capponi and Charles-Albert Lehalle - A comprehensive guide to contemporary practices in machine learning and data sciences for financial markets.

- Machine Learning in Finance: From Theory to Practice by Matthew F. Dixon, Igor Halperin, and Paul Bilokon - Covers the theory and practice of applying machine learning in finance.

- Machine Learning For Financial Engineering by László Györfi, György Ottucsák - Focuses on the application of machine learning techniques in financial engineering.

Mathematical Optimization and Stochastic Calculus

- Convex Optimization by Stephen Boyd and Lieven Vandenberghe - A detailed guide on convex optimization techniques used in finance.

- Financial Calculus by Martin Baxter and Andrew Rennie - An introduction to derivatives pricing using stochastic calculus.

- Stochastic Calculus for Finance I by Steven Shreve - Introduction to stochastic calculus for financial modeling.

- Stochastic Calculus for Finance II by Steven Shreve - Advanced concepts in stochastic calculus for complex financial models.

- Optimization Methods in Finance by Gérard Cornuéjols and Reha Tütüncü - Introduces optimization techniques and their applications in finance.

- Kalman Filtering: with Real-Time Applications by Charles K. Chui and Guanrong Chen - A practical guide to the application of Kalman filtering in real-time systems.

Portfolio Management and Financial Instruments

- Modern Portfolio Theory and Investment Analysis by Elton et al. - An in-depth look at Modern Portfolio Theory and its practical applications.

- Options, Futures, and Other Derivatives by John Hull - Essential reading on derivatives trading.

- Asset Management: A Systematic Approach to Factor Investing by Andrew Ang - Discusses a systematic approach to factor investing.

- Portfolio Management under Stress: A Bayesian-Net Approach to Coherent Asset Allocation by Riccardo Rebonato and Alexander Denev - Focuses on portfolio management strategies under stressful market conditions.

- Quantitative Equity Portfolio Management by Ludwig Chincarini and Daehwan Kim - Advanced techniques focused on quantitative equity portfolio management.

Volatility Analysis and Options Trading

- Volatility and Correlation by Riccardo Rebonato - Discusses volatility and correlation in financial markets and their use in risk management.

- Study Guide for Options as a Strategic Investment by Lawrence McMillan - A comprehensive analysis of options strategies for various market conditions.

- Volatility Trading by Euan Sinclair - Practical strategies for trading volatility.

- The Volatility Surface by Jim Gatheral - Properties of the volatility surface and its implications for pricing derivatives.

- Dynamic Hedging: Managing Vanilla and Exotic Options by Nassim Nicholas Taleb - Introduces dynamic hedging strategies and their applications in managing standard and exotic options.

Python and Programming

- Python for Finance by Yves Hilpisch - Essential techniques for algorithmic trading and derivatives pricing.

- Python for Algorithmic Trading: From Idea to Cloud Deployment by Yves Hilpisch - Comprehensive guide on implementing trading strategies in Python, from data handling to cloud deployment.

- Python for Finance Cookbook - Second Edition by Eryk Lewinson - Over 80 powerful recipes for effective financial data analysis, using modern Python libraries such as pandas, NumPy, and scikit-learn.

- Python for Data Analysis by Wes McKinney - Written by the creator of the Pandas library, this book is essential for financial data analysis.

Biographies

- The Man Who Solved the Market: How Jim Simons Launched the Quant Revolution by Gregory Zuckerman - The unbelievable story of Jim Simons, a secretive mathematician who pioneered the era of algorithmic trading and made $23 billion doing it, whose Renaissance's Medallion fund has generated average annual returns of 66 percent since 1988.

- Poor Charlie's Almanack: The Essential Wit and Wisdom of Charles T. Munger by Charles T. Munger, Peter D. Kaufman (Editor), Warren Buffett (Foreword), John Collison (Foreword) - This book offers lessons in investment strategy, philanthropy, and living a rational and ethical life.

- More Money Than God: Hedge Funds and the Making of a New Elite by Sebastian Mallaby - Details the history of hedge funds and their impact on financial markets.

Research Papers

Seminal and recent research that advances the field of quantitative finance.

Foundational

- Advances in Financial Machine Learning by Marcos Lopez de Prado - Addresses the key challenges of applying ML to finance, including backtest overfitting and feature importance.

- Deep Learning for Asset Pricing by Luyang Chen, Markus Pelger, and Jason Zhu - Uses deep neural networks to estimate conditional asset pricing models.

- Empirical Asset Pricing via Machine Learning by Shihao Gu, Bryan Kelly, and Dacheng Xiu - Comprehensive comparison of ML methods for measuring risk premiums.

Market Microstructure and Regime Detection

- Identifying States of a Financial Market - Statistical methods for financial market state identification.

- Memory Effects in Stock Price Dynamics - Analyzes long-memory and persistence phenomena in stock price dynamics.

AI Agents for Trading

- TradingAgents: Multi-Agents LLM Financial Trading Framework by Xiao et al. (2024) - Multi-agent LLM framework simulating trading firm dynamics with specialized analyst and trader roles.

- FinAgent: A Multimodal Foundation Agent for Financial Trading by Zhang et al. (2024) - Tool-augmented multimodal agent processing numerical, textual, and visual market data.

Original Research and Notes

In-depth analysis and strategy implementation guides maintained as part of this project.

Strategy Implementation (book/myquant/)

An 8-chapter bilingual (EN/CN) quantitative trading strategy guide with Python implementations:

- Chapter 1: Trend Following Strategies - Moving averages, channel breakouts, momentum indicators.

- Chapter 2: Mean Reversion Strategies - Pairs trading, statistical arbitrage, cointegration.

- Chapter 3: Arbitrage Strategies - Cash-futures arbitrage, convertible bond arbitrage, ETF arbitrage.

- Chapter 4: High-Frequency Trading - Market making, order flow prediction, latency arbitrage.

- Chapter 5: Machine Learning Strategies - Random forests, LSTM, reinforcement learning for trading.

- Chapter 6: Fundamental Quant Strategies - Fama-French factors, multi-factor models, event-driven quant.

- Chapter 7: Volatility Strategies - GARCH modeling, volatility surface, variance risk premium.

- Chapter 8: Options Strategies - Delta neutral, Greeks, dynamic hedging.

- Full Strategy Taxonomy (TOC) - Complete knowledge framework for quantitative trading strategies.

Research Essays (think/)

- HMM Quantitative Trading Strategy: An Overview - Hidden Markov Models for regime detection and dynamic risk allocation, inspired by Renaissance Technologies.

- Markov-Switching Model Application - Regime-switching regression models combining traditional statistics and machine learning for market state prediction.

- Dynamic Financial Modeling Using Fuzzy Systems - Fuzzy systems theory applied to transform technical trading rules into price dynamics models.

- AI-Agent Trading - Survey of LLM-based multi-agent trading frameworks (TradingAgents, FinAgent).

Book Notes

- Systematic Trading by Robert Carver - Detailed notes on systematic strategy design: forecasting, position sizing, portfolio allocation, and risk management.

Community and Conferences

Communities, forums, and conferences dedicated to quantitative finance and AI in trading.

Communities

- QuantConnect Community - Active forum for algorithmic trading discussions with shared strategies and research.

- Quantopian Legacy (QuantPedia) - Database of quantitative trading strategies from academic research.

- r/algotrading - Reddit community for algorithmic trading discussion and resource sharing.

- r/quant - Reddit community for quantitative finance professionals and students.

- Wilmott Forums - Long-running quantitative finance community with deep technical discussions.

- Nuclear Phynance - Forum for quantitative finance practitioners focusing on derivatives and risk.

Conferences

- The Trading Show - Conference covering algorithmic trading, market structure, and fintech innovation.

- QuantMinds - Global conference series covering quantitative finance, risk management, and AI applications.

- AAAI Conference on AI in Finance - Academic conference featuring AI/ML research applied to financial markets.

- ACM ICAIF - ACM International Conference on AI in Finance, bridging CS and finance research.

Related Lists

- awesome-quant - Curated list of libraries, packages, and resources for quants, organized by programming language.

- awesome-ai-in-finance - Resources for AI applications in the financial industry.

- awesome-systematic-trading - Curated list of systematic trading tools and strategies.

- awesome-deep-learning - Curated list of deep learning tutorials, projects, and communities.

Reference

- 46 Awesome Books for Quant Finance, Algo Trading, and Market Data Analysis - Comprehensive book list from PyQuant Newsletter.

- 10 Awesome Books for Quantitative Trading - Curated reading list for quantitative trading beginners.

- Books for Algorithmic Trading I Wish I Had Read Sooner - Video overview of essential algorithmic trading books.

Contributing

Contributions are welcome! If you'd like to add a resource, fix a link, or suggest an improvement:

- Please ensure your suggestion fits the scope of AI/ML applications in quantitative finance.

- Use the format:

- [Name](url) - Brief description ending with a period. - Add new entries to the most relevant existing section.

- One pull request per resource or a small group of related resources.

- Check that your links are working and not duplicates of existing entries.

For questions, suggestions, or collaboration inquiries:

If you find this project useful, please consider giving it a star. It helps others discover these resources.

Yorumlar (0)

Yorum birakmak icin giris yap.

Yorum birakSonuc bulunamadi